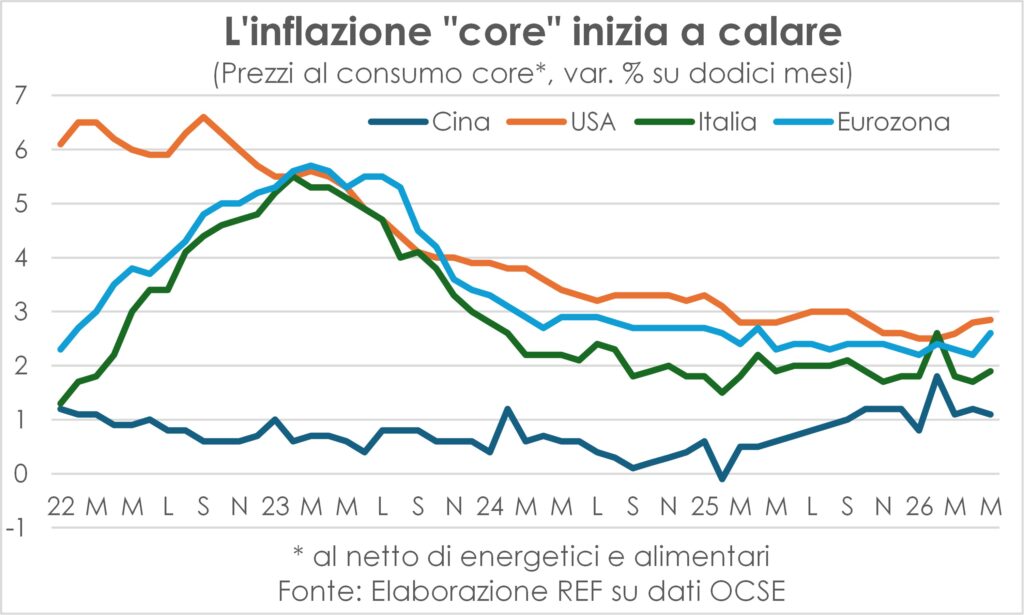

Inflation, evidence of decline

“The belly is no longer there,” Mimmo hummed with relief, turning to the cook Matilde, of African origins and speaking Venetian (the League was yet to come), in a television advertisement from sixty years ago. “Inflation is no more”, they murmur today central bankers At regular meetings and international gatherings—the last one in Sintra, Portugal, from June 29 to July 1—the fear of being overheard and prematurely proclaiming victory. If, indeed, proclaiming victory is fitting for a central banker, more inclined to prudence than exultation.

In fact, the Caution is advised for everyone from the moonlight and missiles that ominously illuminate the Strait of Hormuz, making it at times narrower, or rather occluded by the still unfinished war (wars end when peace is signed: it is not a banality but a protocol), and at times widening it with agreements and ceasefires. And yet, the signs and evidence there is a return of the dynamics of the consumer prices at the pre-war pace. Let's see them.

First of all, the June data indicate the beginning of thelowering of temperature of the prices paid by consumers (only that, while the African heat waves continue to hit Europe). In theEurozone we went from 3,2% in May to 2,8%; in USA The Cleveland Fed forecasts a reduction to 3,9% from 4,2% (and to 3,7% in July, but it is still a very volatile number). UK It has already remained stable in May, rather than rising as feared, and is expected to fall. Japan, plagued and bent by a deflation that lasted almost half a human lifetime (it began in the early 90s of the last century), rose in May to 1,5% from 1,4%, but the super-core one fell from 1,9% to 1,8%. In China, another country with a whiff of deflation, fell to 1% in June, from 1,2% in May, and the core itself marked +1%.

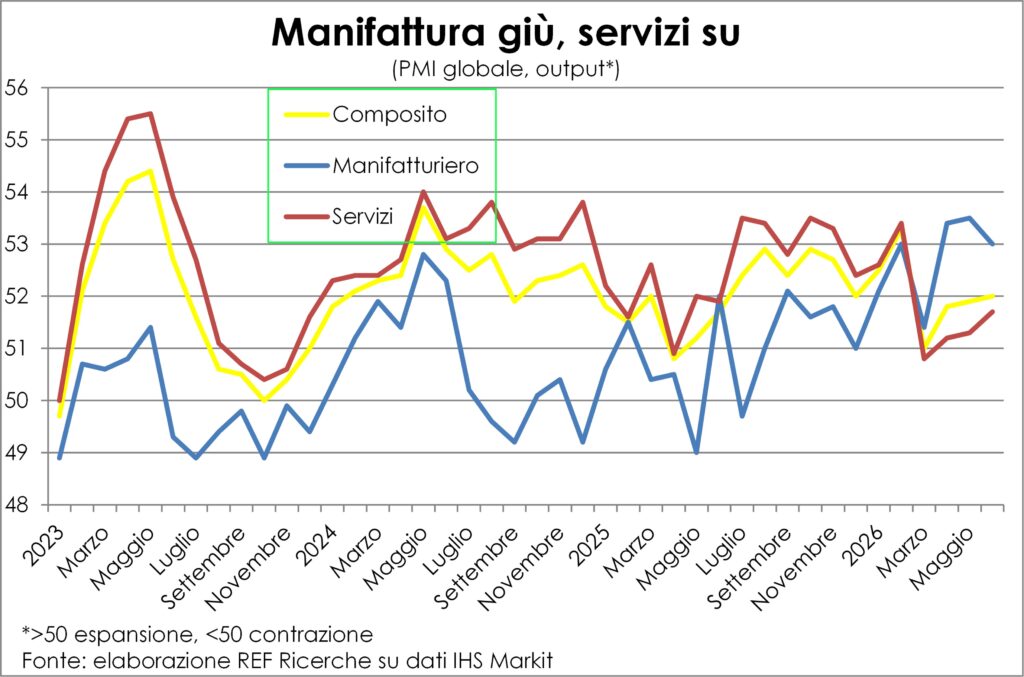

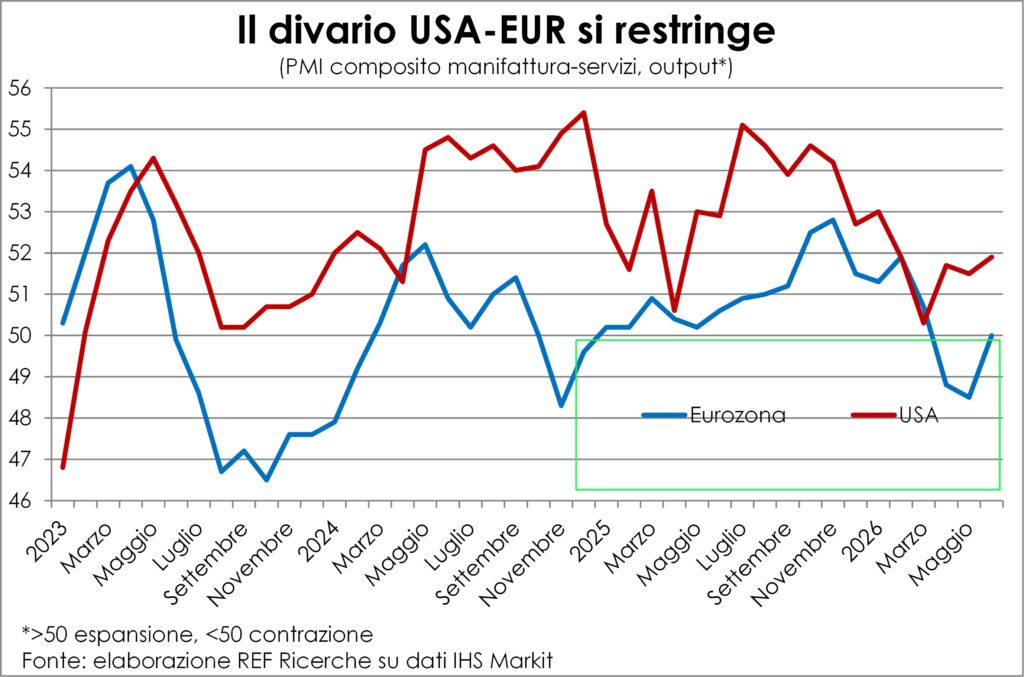

Also the price component of the PMI survey It points to a sharp slowdown (which does not mean a reversal, at least not yet) in increases in both the prices paid for inputs and the prices received for output, in the manufacturing and services sector combined and also in the two sectors taken separately.

But how come, it's already over much-feared new inflationary surge, which forced central bankers, stung by the late intervention in 2022, to rush to preemptively address the situation with words and deeds? And was that all there was to it? What happened, and what will happen?

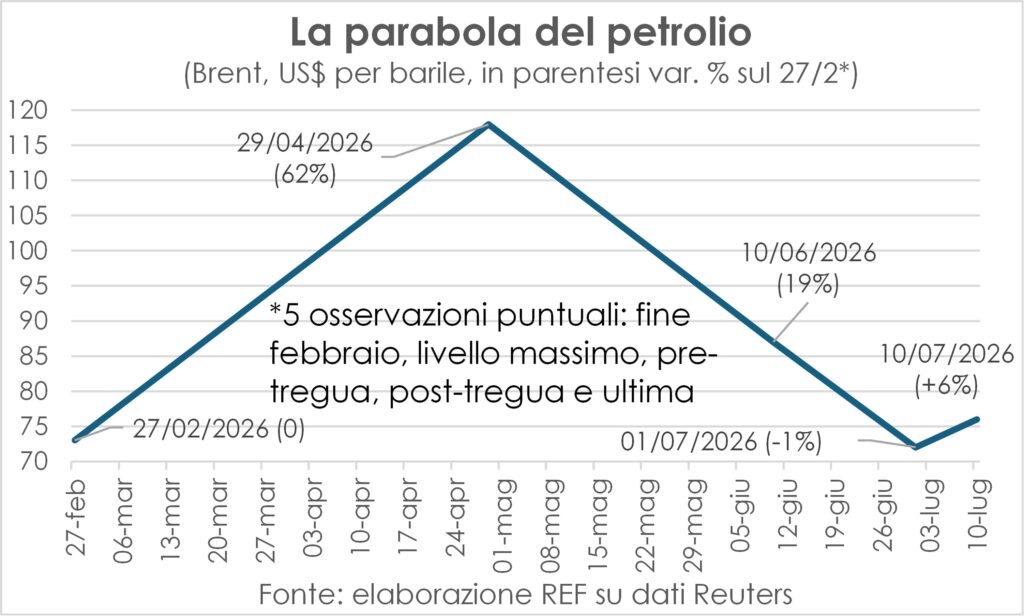

The parable of oil

Certainly among the reasons for the aborted inflationary wave there is the brevity of the war-energy shock, which began in late February and ended in the second half of June, with the signing of the memorandum of understanding, the ceasefire, and the reopening of the Strait. Thus, the prices of oil and its derivatives, which had skyrocketed, fell back to where they were until February 29th, completing a nearly perfect parabola, only to then rise by 6% when the two belligerents began exchanging ballistic pleasantries again. But a +6% is obviously lower than the +62% reached on April 29th, and is far from the N% that would have been achieved if oil had skyrocketed 200+ dollars which many had considered a sure consequence of the third Gulf War. However, the 6% increase cannot be classified as a shock.

The brevity meant that there was almost no time to get the complex mechanism of second-round effects, which end up involving wages in a vicious spiral, a spiral that central bankers always aim to to cut off and put to sleep, although they are not animated by evil purposes like Count Uncle.

Already, wages: I am the first mobile engine of any real inflationary process. Not that it is the only one. In the distribution of income, too, gross operating result It has a significant weight, but it usually does not push prices up unless exceptional cases, that is, of very, very strong question and extreme scarcity of immediate supply; otherwise companies tend to adjust production upwards to gain or at least maintain market share, for retain customers who do not want to pay more for the products, because they would be capable of turning to a competitor.

Curtailing wages and rampant uncertainty

In the current context, neither wages are moving much nor is demand extraordinarily lively; on the contrary, wages continue their long slowdown and the question remains intimidated by the enormous uncertainty triggered by the "pranks" Mr. Trump (in the true sense, as he resembles the good Manzonians in his ways), as well as the difficulty consumers are having in dealing with the loss of purchasing power caused by the higher energy bill. It is no coincidence that his pranks and bills have sent their confidence.

The big differences with 2021-22

In short, the current conditions are very different from those of 2021-22, when the supply bottlenecks, combined with a really voracious final question and a salesman's job market, they did both expand profit margins both trigger compensatory wage increases.

Therefore the Governor of the Bank of Italy did more than well, Fabio Panetta, to remember these great differences (“This is not a replay of 2022”, he declared while speaking in Frankfurt on 7 July), to avoid the ECB making the mistake of raising rates again; although that same experience has reawakened the business readiness in adjusting price lists to higher costs, a readiness that the very long phase of great moderation of prices and costs had numbed (Panetta has well underlined this).

The forces that can push prices down

However, there is room for some optimism. If the two contenders, the US and Iran, stopped playing with weapons (a big "if" given the macho psyche of both), inflation could go down much more quickly than expected. Not only thanks to the recovery in the prices of energy raw materials and their derivatives, but also due to the rewind the effects that the war shock has had on manufacturing companies and on those providing consumer services, specifically travel and tourism.

We'll talk about rewinding later. Here we point out that the accumulated inventories in manufacturing to avoid being left without inputs (as in 2021-22) they risk being excessive and will have to be disposed of; in the PMI surveys we read that companies have started to reduce purchases for empty the warehouses, and soon they will have to promote sales with discounts. Discounts that even tertiary businesses in the travel and hospitality sectors will begin to do to reduce the damage to the tourist season and fill planes and hotels. Adding the reduction in energy prices to these discounts, in the coming months we could see consumer prices falling, not just slowing.

Between the stars and the stables

What goes up must come down, Isaac Newton famously said, and the English in the 800th century made it a saying that transferred the law of gravity from the world of physics to that of human fortunes and events (or, in Bertoldo's version, "He who throws a stone high, will come back to hit his own head"). In economics It doesn't quite work like that, as demonstrated by the increase in well-being in humanity as a whole over the last two and a half centuries (despite very large inequalities and enormous fluctuations). However, sometimes it works exactly like this, even vice versa, that is what goes down must come back upWhat we are experiencing is one of those rare occasions.

The war-energy shock, in fact, has sent to the stars manufacturing activity and in the stables service activities. Given the different nature of the products of the two, because in one there is a temporal separation between supply and demand and in the other there must almost always be a coincidence, industrial companies have been able to activate demand and production for the warehouse, in order to avoid finding ourselves in the situation experienced just five years ago of shortages of raw materials and semi-finished products and soaring costs and delays in deliveries. Only that this strategy of just in case It itself caused the supply bottlenecks and price increases that were intended to be avoided and it proved to be defective for excess of foresight.

The rewind has started

In fact, the rather rapid reopening of the Strait of Hormuz (assuming that the new clashes are temporary) nullifies that effort and now the accumulated stocks risk proving to be excessive, so that many companies, according to PMI surveys, began to reduce purchases To clear excesses, shifting supply and demand in the opposite direction. As the destocking spreads, global manufacturing will see declines in orders and output, mirroring what happened between March and May and, to some extent, June.

In reverse, services have suffered The immediate impact of rising transportation costs on consumer demand (jet fuel prices fluctuated twice as much as crude oil) and on transportation in general, thus penalizing their business. Now, the situation will rebound, symmetrically.

Rotation between countries

Together with and, in many ways, as a consequence of the rewinding of the effects on the sectors of the “three-month shock”, rotation between countries is taking place and will gain strength. Depending on the greater dependence from abroad for primary energy sources and the largest intensity tourism of their respective economies.

Of course Europe, and in particular theEuro area, possess both characteristics. So it was hit both on the supply side, with the sharp increase in costs and the risk of energy rationing – by the way, for weeks if not months there have been analyses published on this risk and on the destruction of energy needs to face a summer and perhaps an autumn with few supplies of oil and gas, and derivatives: now a deathly silence has fallen on both –, both on the demand side, internal and external. Internal, because families and businesses, crushed between the anvil of uncertainty and the hammer of price increases, have cautiously moderated spending. Foreign, because airfares on long routes had become too high for a very crowded segment of Asian tourists who aspire to get to know the Old Continent much more than they wish to visit the New, already so similar to the very modern cities they inhabit and to which they are accustomed.

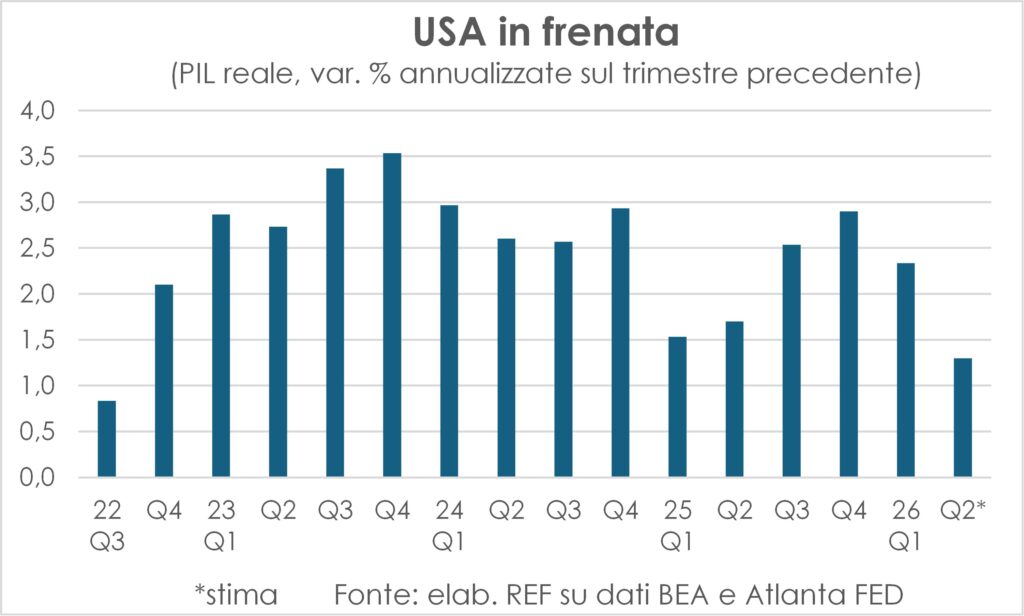

On the contrary, the penalty for the USA there was one for internal demand (consumers had to recalibrate their spending based on the high energy prices) but not as a country, which actually saw improved terms of trade, being a net exporter of oil and gas. There was no foreign demand, for the reason stated above and having actually benefited from the inflows of fans at the soccer World CupHowever, the star-spangled giant has grown at a steady pace over the last three quarters. slower pace from 2022 (+1,3% annualized on average), and the epicenter of the slowdown is in the consumption (+1,5%), while the AI-related investments (plants and machinery +12,2% and intangible assets +8,5%); on the other hand, as highlighted in the latest Lancette, the creation of jobs in April and May it was “doped” by the revision of the seasonality coefficients, while real wages decreased.

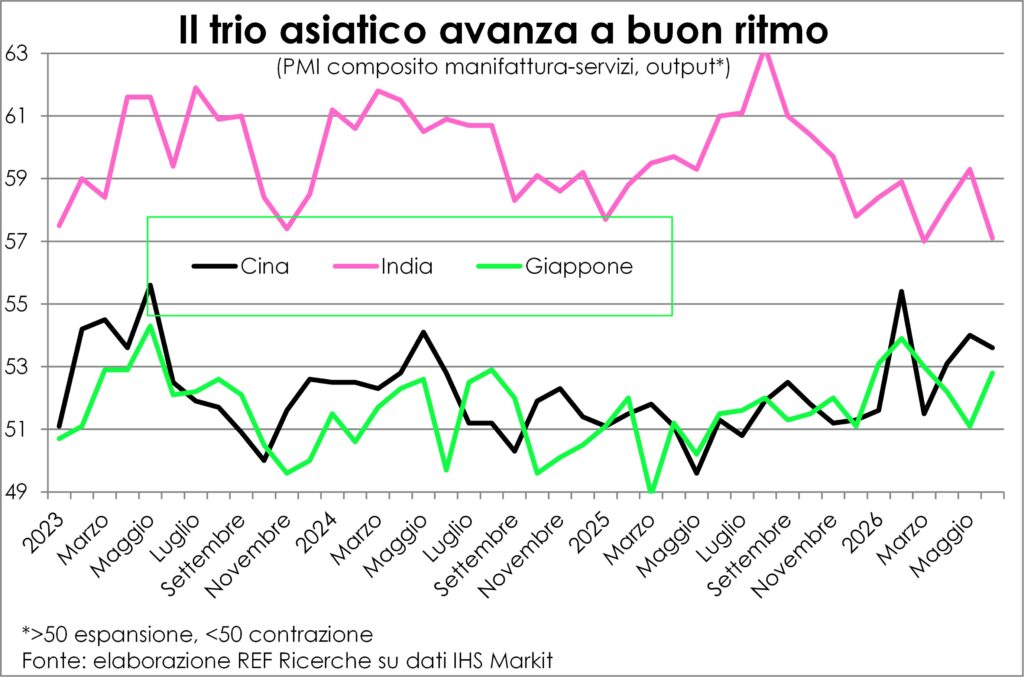

And theAsia? In general the economies of the first continent by demographic size (60,2% of the world total) and economic size (45,6%) they earn from rewinding and rotation, because they are dependent on imported energy and because they are very manufacturing but they are also in this true hub of goods needed for the AI revolution. Moreover, internal distances are such that the reduction in airfares will give new impetus to intracontinental travel, in addition to the intercontinental ones already mentioned above.

If we look at the three major Asian economies, we observe a loss of pace in India (still high), an acceleration in Japan and greater Chinese vivacity. engine of the world convoy he's in that trio.

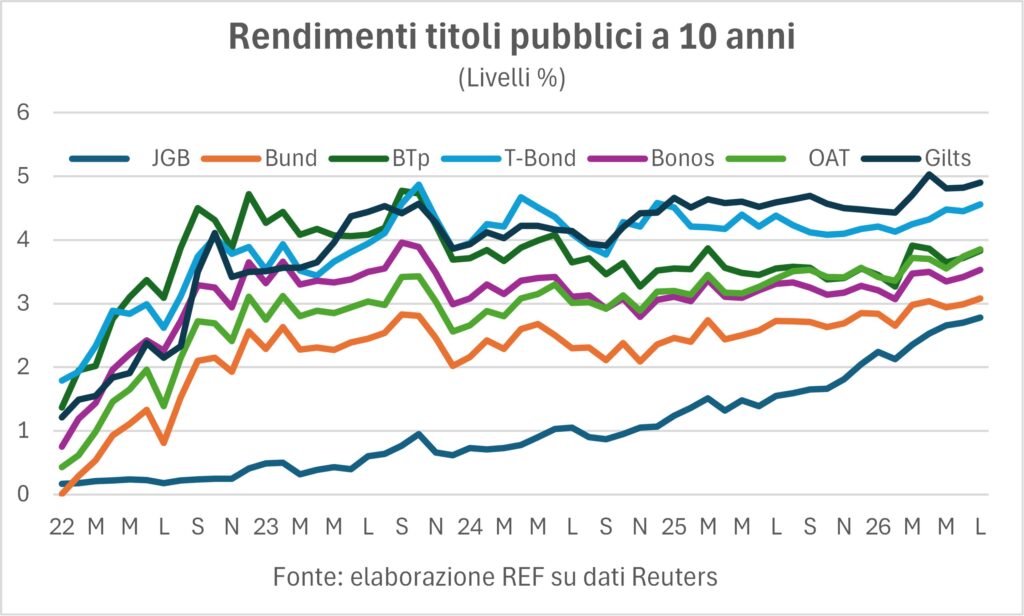

Rates rise, in space and time

In June, in a span of a few days, there were two big news: on the one hand, a first chord, however fragile and called into question today, on the reopening of the Strait of Hormuz, an agreement which was followed by a sharp reduction in the price of crude oil, only partially reversed now; on the other hand, the first meeting of the Fed under the new presidency of Kevin Warsh, with no progress made on the level of the key interest rate, but with a firm reaffirmation of the fight against inflation.

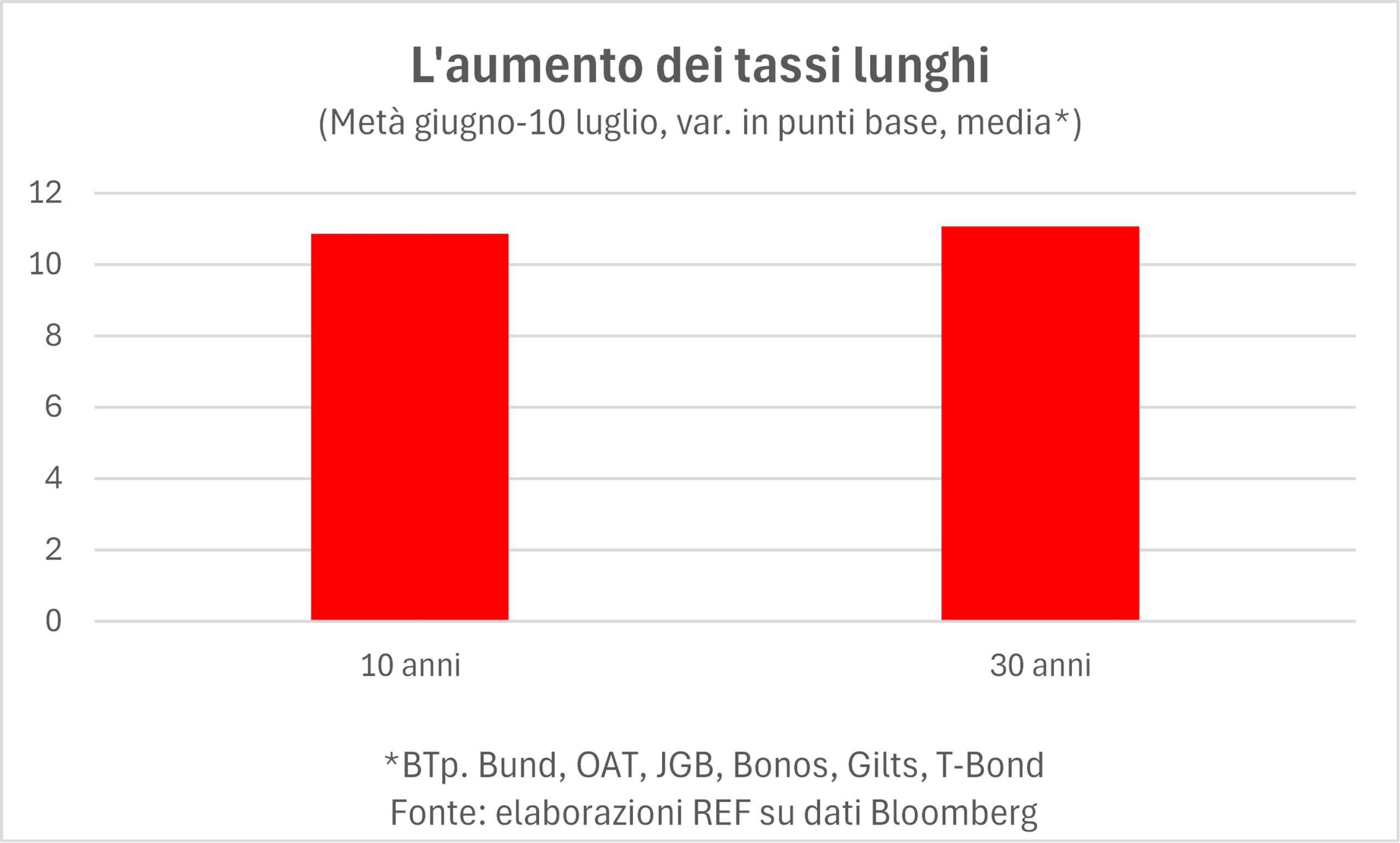

The first novelty was supposed to support the doves: less inflation = lower rates. The second was interpreted by the markets as a greater probability of rate hike, given that we are far from the famous 2% target. So, what happened to rates from mid-June to today? Let's look at the seven major bond markets in the West (with Japan being the 'honorary Western', and in any case, 'seeking the east through the west' brings us to Japan...): T-Bonds, Bunds, Gilts, BTp, OATs, Bonos and JGBs. What happened was that the hawks' anxieties have prevailed on the hopes of the doves: yields have increased, albeit slightly, everywhere, and, what is more worrying, they have increased on longer deadlines (30 years) as much as 10-year yields.

It is always difficult to scrutinize the market motivations; if it is true that the bullish desires of many members of the FOMC – the body of the Fed that takes monetary policy decisions – should not, in themselves, have influenced the outlook for rates in other markets, then there should be other motivations for rate increases that extend in space and timeWe have illustrated these reasons several times in the past: need for investments, public and private. The yields of government bonds reflect the fact that the investments made necessary by the various transitions – digital and environmental – weigh heavily on the public sector, not to mention the costs for defenseBut the investment needs of the private sector are no less important.AI, unlike other industrial revolutions, needs, before being put into practice, huge outlays on capital account, here and now. It's a bit as if, to return to the first industrial revolution, it had first been necessary to manufacture millions and millions of steam engines, and then distribute them, across space and time, so that those who received them could benefit from the increased productivity.

As mentioned, these investment needs have been evident for some timeWhy, it seems, have they come to weigh more heavily on returns than before? There's always a moment—unpredictable—when the market "realizes" that a factor—like the financing required for huge investments—must be taken seriously, and it acts accordingly.

The underlying inflation (excluding food and energy) remains fairly stable, and so do the inflation expectations (as revealed by the difference between the yields of indexed and non-indexed bonds), which had increased at the outbreak of the war, have since declined from those levels. The problem lies in the fact that increases in nominal rates are transmitted live on real ratesIn Italy and France, these exceed 2%, which certainly doesn't help growth that remains at 'point zero'.

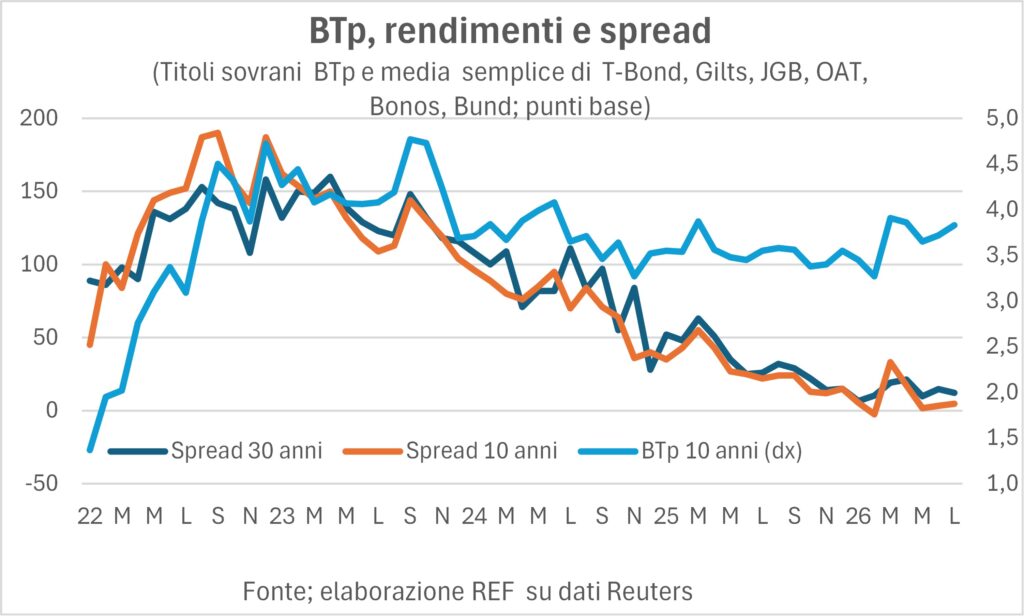

As happens in times of rising interest rates, the BTP spread They are suffering from it, even if they remain close to the record low levels reached in February, just before the US-Israeli attack on Iran.

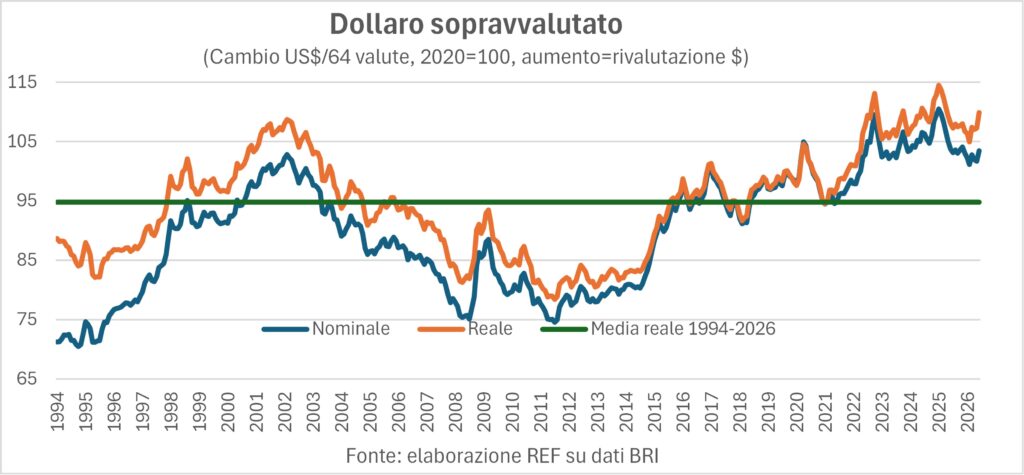

The dollar strengthens

La US currency is tossed around from cyclical and structural factors. Sometimes one prevails, sometimes the other. Structurally, the dollar is overratedIts effective exchange rate, both nominal and real, is significantly higher than the long-term average (see graph), and this appreciation undermines the competitiveness of Made in USA products and encourages imports. The consequences? trade deficit American continues at high levels, despite the tariffs, and the net foreign position (assets minus liabilities) of the United States is frighteningly negative, at 73% of GDP (for comparison, in Italy it is largely positive).

But, with every rustle of economic factors, the weight of fundamentals lightens: it was enough for the new Fed Chairman to reiterate the belief that 'inflation will not pass' for the markets to become convinced that key interest rates will increase and lead the dollar towards strengthening, based on a prospective increase in the interest rate differential between the US and the rest of the world. This reaction was much broader because, as we know, Kevin Warsh had been appointed by Trump with a mandate – not expressed in a whisper – to lower rates.

The other salient fact in the currency markets is the persistent yen weaknessIn the past, we've highlighted how the devaluation of the Japanese currency had resoundingly disproved a close correlation with the spread between US (T-Bond) and Japanese (JGB) yields. When this spread widened, it was more profitable to invest in America, and the exodus of capital weakened the yen. But, for the past year, the opposite has happened. sharp rise in Japanese rates has narrowed the differential significantly, and despite this, the yen has devalued (against the dollar) to levels not seen in forty years. The causes? One could argue that, even if the differential has narrowed, for Japanese capital it continues to be it is convenient to invest in T-Bonds. But the main reason seems to be another. It has resumed carry trade, that is, borrowing in the currency with low interest rates to invest in the one with high interest rates. It is true that the convenience of the carry trade has shrunk, however many investment funds have started borrowing in yen again to buy higher-yielding dollars. carry trade It is not a niche procedure: it covers a large portion of the turnover in the currency market.

The Stock Market Between Wars and Bubbles

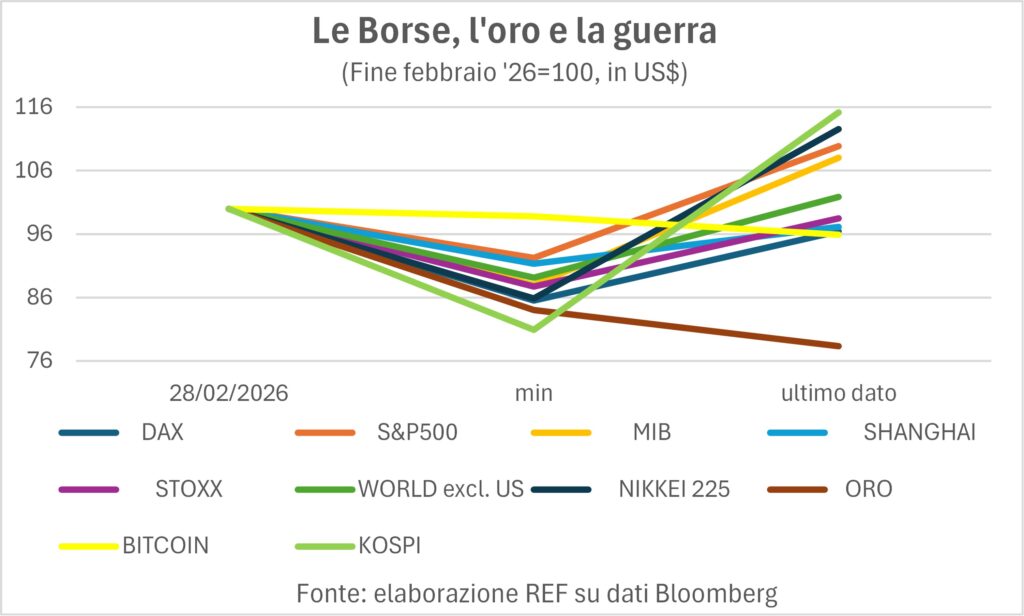

After the incident at the end of February, the stock markets (plus a safe haven like the and a good 'color can that runs away' like the Bitcoin) were understandably scared, and everyone dropped, with Bitcoin dropping by 1% at its nadir to South Korea's Kospi dropping by 20%. And today?

Compared to the starting level, we divide the nine activities painted in the graph between those that remain below the initial level and those that have exceeded it more or less abundantly. The data show the combined effect of prices and exchange rates: the indices have all been translated into dollars. By far thelast place goes to the yellow metal, which is probably paying for the strong upward surge of the last eighteen months. Below the pre-war figure are also – but with modest reductions, from -1 to -4% – the DAX German, the Bitcoin and the index of the Chinese stock exchange (SHCOMP.IND). Let's get to the head of the platoon: in first place it's the legendary Kospi, followed by the Nikkei225, from S & P500, from our Eb and from the MSCI index 'world excluding the USA'. So what does the 'wisdom of crowds' tell us? It tells us that the Gulf War it didn't hurt confidence and hopes too muchMarkets continue to shrug their shoulders in the face of wars and bubbles. Greeting...